Filing an Income Tax Return (ITR) has become significantly easier in recent years thanks to pre-filled forms, online filing systems, and automated reporting by banks, employers, mutual funds, brokers, and other financial institutions. However, while the filing process may seem straightforward, even a small reporting error can attract the attention of the Income Tax Department.

Today, tax authorities have access to vast amounts of financial information through systems such as Form 26AS, the Annual Information Statement (AIS), and the Taxpayer Information Summary (TIS). These tools allow authorities to cross-check the income and transactions reported by taxpayers against information submitted by employers, banks, stockbrokers, mutual fund houses, and other reporting entities.

As a result, discrepancies that once went unnoticed are now identified much more quickly.

Receiving a tax notice does not necessarily mean wrongdoing. In many cases, notices are generated simply because information reported in an ITR does not match official records. Understanding the most common mistakes can help taxpayers avoid unnecessary scrutiny, delayed refunds, and compliance issues.Here are seven ITR mistakes that frequently trigger tax notices.

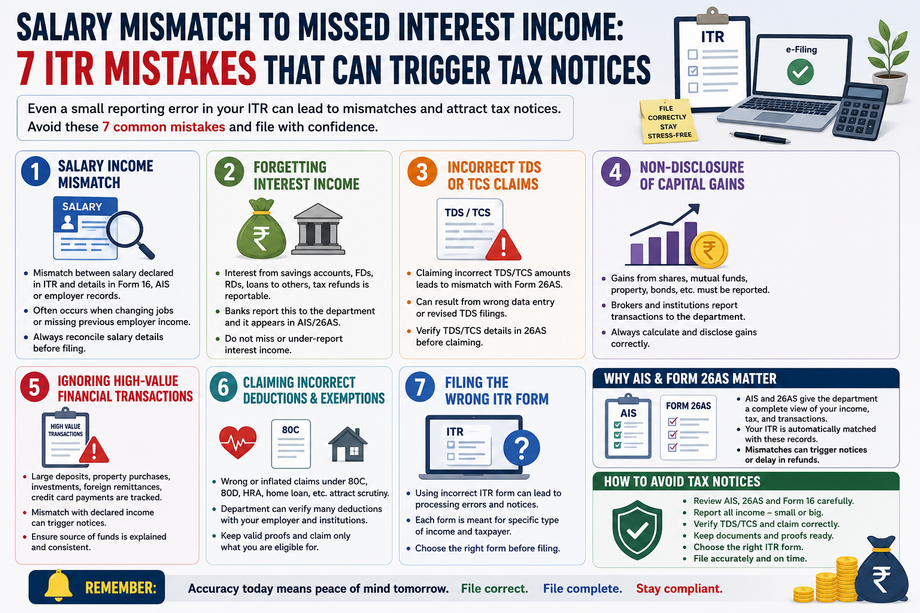

1. Salary Income Mismatch

One of the most common reasons taxpayers receive notices is a mismatch in salary income.

Many salaried individuals assume that the salary information shown in their Form 16 is sufficient for filing. However, discrepancies can arise when employees change jobs during the financial year or fail to disclose income from previous employers.

The Income Tax Department compares salary details reported in the ITR with information available from Form 16, TDS returns filed by employers, and data reflected in AIS.

If the salary declared in the return is lower than the amount reported by employers, authorities may seek clarification regarding the difference.

To avoid problems, taxpayers should carefully reconcile salary income across all relevant documents before filing.

2. Forgetting Interest Income

Many taxpayers unintentionally overlook interest income because they assume that tax has already been deducted or because the amount appears insignificant.

However, interest earned from savings accounts, fixed deposits, recurring deposits, corporate deposits, and even income tax refunds is generally reportable.

Banks and financial institutions routinely report such income to tax authorities. As a result, unreported interest often appears as a mismatch between the ITR and AIS.

Even relatively small amounts can trigger automated scrutiny if they remain undeclared.

Taxpayers should review all interest-related entries before submitting their returns.

3. Incorrect TDS or TCS Claims

Tax Deducted at Source (TDS) and Tax Collected at Source (TCS) credits help reduce tax liability. However, claiming credits that do not match official records can create problems.

Errors may occur due to:

-

Incorrect data entry

-

Mismatched figures

-

Delayed reporting by deductors

-

Duplicate claims

The Income Tax Department compares TDS and TCS claims with Form 26AS and AIS records.

If a taxpayer claims higher credits than those reflected in official records, the department may adjust refunds or issue a notice seeking clarification.

Reviewing Form 26AS before filing remains one of the simplest ways to prevent such issues.

4. Non-Disclosure of Capital Gains

The popularity of equity investing, mutual funds, and digital trading platforms has increased significantly in recent years.

Unfortunately, many investors fail to properly report capital gains arising from:

-

Share sales

-

Mutual fund redemptions

-

Property transactions

-

Bond sales

-

Other capital assets

Many of these transactions are automatically reported by intermediaries and reflected in AIS.

Taxpayers sometimes assume that because securities transaction tax has been paid, additional reporting is unnecessary. Others mistakenly report sale proceeds without calculating actual gains.

Both situations can create discrepancies.

Capital gains should always be calculated accurately and disclosed under the appropriate income head.

5. Ignoring High-Value Financial Transactions

The tax department receives information about numerous high-value financial activities through the Statement of Financial Transactions (SFT) reporting framework.

The tax department closely monitors high-value financial transactions through various reporting mechanisms. Large cash deposits, property purchases, mutual fund investments, foreign remittances, and significant credit card payments are often reported automatically.

If these transactions do not align with the income declared in your ITR, authorities may seek an explanation. Many taxpayers are unaware that such transactions are reflected in AIS. Ignoring them can create red flags during tax assessment. Maintaining proper documentation regarding the source of funds is important. Ensuring consistency between your financial activities and reported income helps reduce the risk of notices and inquiries.

Examples include:

-

Large bank deposits

-

Significant mutual fund investments

-

Property purchases

-

Property sales

-

High-value credit card payments

-

Foreign remittances

-

Major securities transactions

When these transactions appear in AIS but are not adequately supported by declared income, they may trigger scrutiny.

Authorities may seek explanations regarding the source of funds used for these activities.

Taxpayers should ensure that all major financial transactions are consistent with their reported income and financial profile.

6. Claiming Incorrect Deductions and Exemptions

Tax deductions help taxpayers legally reduce their taxable income, but incorrect claims can attract scrutiny. Common errors include overstating Section 80C investments, claiming HRA without supporting evidence, or entering incorrect health insurance deduction amounts under Section 80D. The tax department can verify many deductions using information received from employers and financial institutions.

If discrepancies are identified, taxpayers may be asked to provide proof. Unsupported or inflated claims can lead to penalties and additional tax demands. Keeping investment receipts, insurance premium records, and rent documents safely stored is essential for supporting deduction claims during assessment.Deductions help reduce taxable income, but incorrect claims often attract attention.

Common problem areas include:

-

Section 80C deductions

-

Health insurance deductions under Section 80D

-

House Rent Allowance (HRA) exemptions

-

Home loan benefits

-

Other tax-saving claims

Some taxpayers mistakenly claim deductions without maintaining supporting documents. Others enter incorrect amounts while filing.

The Income Tax Department may compare deduction claims with information reported by employers and other institutions.

If inconsistencies emerge, taxpayers may be asked to provide evidence supporting their claims.

Maintaining proper records remains essential.

7. Filing the Wrong ITR Form

Choosing the incorrect ITR form is another surprisingly common mistake.Different forms are designed for different categories of taxpayers and income sources.For example, individuals earning only salary income may qualify for one form, while taxpayers with capital gains, foreign assets, business income, or multiple income streams may require another.Using an incorrect form can lead to processing issues, invalid returns, or requests for correction.Taxpayers should carefully review eligibility criteria before selecting an ITR form.

Why AIS and Form 26AS Matter More Than Ever

AIS (Annual Information Statement) and Form 26AS have become essential tools for tax compliance. These documents provide a consolidated view of your financial transactions, including salary income, interest earnings, dividends, TDS credits, securities transactions, and high-value purchases.

The Income Tax Department uses this information to verify the accuracy of returns filed by taxpayers. Any mismatch between your ITR and these records can trigger automated scrutiny. Therefore, reviewing AIS and Form 26AS before filing has become a crucial step. These documents help taxpayers identify errors early and ensure that all income and tax credits are reported correctly.

Modern tax compliance is increasingly data-driven.

AIS, TIS, and Form 26AS provide tax authorities with a comprehensive picture of a taxpayer’s financial activities.

These systems capture information related to:

-

Salary income

-

Interest earnings

-

Dividend income

-

Capital gains

-

Property transactions

-

Securities trades

-

High-value purchases

-

Foreign transactions

Because this information is available electronically, mismatches are detected more efficiently than ever before.

Experts therefore recommend reconciling all financial records against AIS and Form 26AS before filing an ITR.

How to Avoid Tax Notices

Avoiding tax notices largely depends on accuracy and transparency while filing your return. Taxpayers should reconcile salary details, interest income, capital gains, and tax credits with official records before submission. Reviewing AIS, TIS, and Form 26AS helps identify discrepancies in advance. Keeping supporting documents organized is equally important.

Choosing the correct ITR form and verifying all deductions can further reduce compliance risks. It is also advisable to review the return thoroughly before final submission. Taking these simple precautions can help taxpayers avoid unnecessary scrutiny, ensure faster refund processing, and maintain smooth tax compliance.

Although no system can guarantee that a notice will never be issued, taxpayers can significantly reduce their risk by following a few simple practices:

-

Verify salary details using Form 16.

-

Check Form 26AS thoroughly.

-

Review AIS and TIS carefully.

-

Report all interest income.

-

Disclose capital gains accurately.

-

Reconcile TDS and TCS credits.

-

Maintain supporting documents.

-

Choose the correct ITR form.

-

Verify bank account details.

-

Complete return verification after filing.

Most tax notices arise from avoidable reporting errors rather than intentional non-compliance.

Conclusion

Filing an Income Tax Return is no longer just about entering numbers into a form. With sophisticated data-matching systems now in place, accuracy has become more important than ever.

Salary mismatches, missed interest income, incorrect TDS claims, unreported capital gains, undisclosed high-value transactions, unsupported deductions, and wrong ITR forms are among the most common triggers for tax notices.

The good news is that nearly all these issues can be avoided through careful review and reconciliation before filing. Spending a little extra time checking Form 26AS, AIS, TIS, and supporting documents can save taxpayers from future complications, delayed refunds, and unnecessary interactions with the tax department.

In tax compliance, accuracy is often the best defense against unwanted scrutiny.